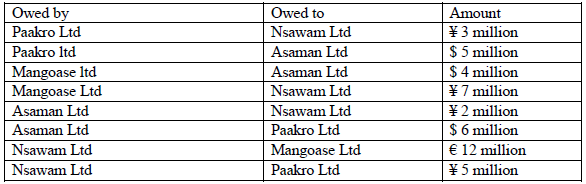

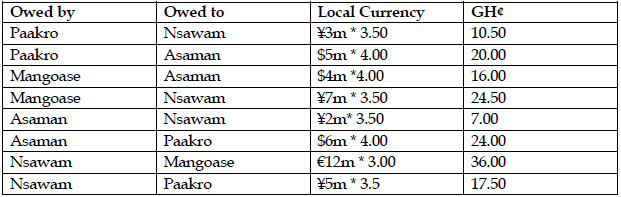

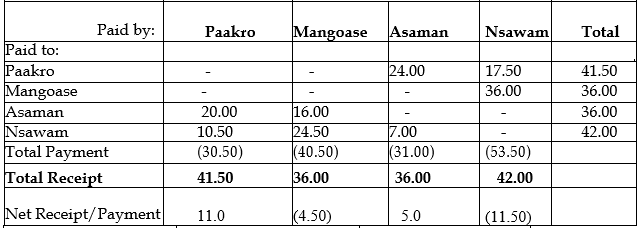

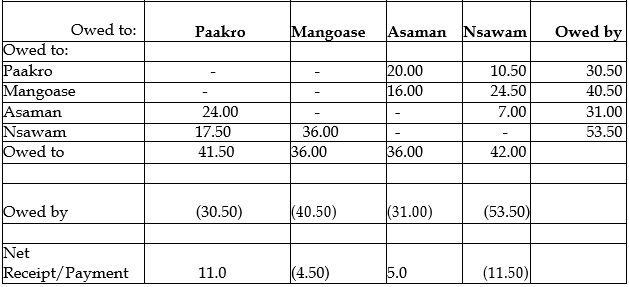

Nov 2017 Q5 b.

The amount of dividends subsidiaries pay to the parent company depend on the parent company’s dividend policies. Again, dividend repatriation represent significant flow for parent companies and contribute to dividend payments.

Required:

Discuss FOUR factors that affect dividend repatriation policies of Multinational Companies. (8 marks)

View Solution

The choice of whether to repatriate earnings from a foreign subsidiary is one of the most important decisions in multinational financial management.

Dividend repatriations represent significant financial flows for parent companies and contribute to dividend payments. The factors that affect dividend repatriation policies can be grouped as follows:

- Financing factors

Repatriation policies may reflect financing concerns of parents who draw on subsidiary cash flows to finance domestic expenses. Two examples of such domestic expenses are dividend payments to external shareholders and capital expenditures in the home countries. - Dividend policy

Dividend repatriations from foreign affiliates may also offer an attractive source of finance for payments of dividends to common shareholders especially when the parent company may prefer a smooth dividend payment pattern and domestic profitability is in decline.

The dividend payments of a subsidiary may also be affected by the dividend policy of the parent company. For example if the parent company operates a constant payout ratio policy, then the subsidiary will have to adopt a constant payout ratio policy too. - Tax regime and dividend payments

Tax considerations are thought to be the primary reason for the dividend policies inside the multinational firm. For example, the parent company may reduce its overall tax liability by receiving larger amounts of dividends from subsidiaries in countries where undistributed earnings are taxed. - Managerial control

Another reason that may determine repatriation policies is the inability to fully monitor foreign managers, especially when affiliates are partially owned.

The desire to control corporate managers around the world carries implications for dividend policies. A multinational firm’s central management can use financial flows within the firm to evaluate the financial prospects and needs of wide-ranging affiliates and to limit the discretion of foreign managers.

It may be sensible to mandate dividend payments to monitor foreign managers, limits their ability to misallocate funds, and to extract returns on investments. - Timing of dividend payments

The timing of payments may also be equally important. For example, a subsidiary may adjust its dividend payments to a parent company in order to benefit from expected movements in exchange rates. A company would like to collect early (lead) payments from currencies vulnerable to depreciation and to collect late (lag) from currencies which are expected to appreciate.

Also given that tax liabilities are triggered by repatriation, these tax liabilities can be deferred by reinvesting earnings abroad rather than remitting dividends to parent companies.

The incentive to defer repatriation is much stronger for affiliates in low-tax countries, whose dividends trigger significant parent tax obligations, than they are for affiliates in high-tax countries – particularly since taxpayers receive net credits for repatriations from affiliates in countries with tax rates that exceed the parent country tax rate.