May 2019 Q2 a&b

Agyemang Boateng has been working with Intellect Consult Limited (ICL) since 2010. At the beginning of January 2016, he was seconded to Accra Metropolitan Assembly (AMA) for a period of six months to be part of a team to spearhead a restructuring exercise and the review of the system of internal controls at the Revenue department of AMA.

Terms of the AMA engagement

ICL was to be paid a one-off settlement of GH¢10,000 at the completion of the engagement as well as reimbursement of monthly operational expenses incurred based on submission of the relevant invoices.

Agyemang’s only entitlements from AMA were the following monthly allowances:

Inconvenience Allowance GH¢ 300

Extra Duties Allowance GH¢ 200

Agyemang’s secondment to AMA did not in any way affect his salary and other entitlements from his employer, ICL, as these continued to accrue to him during the period of the secondment.

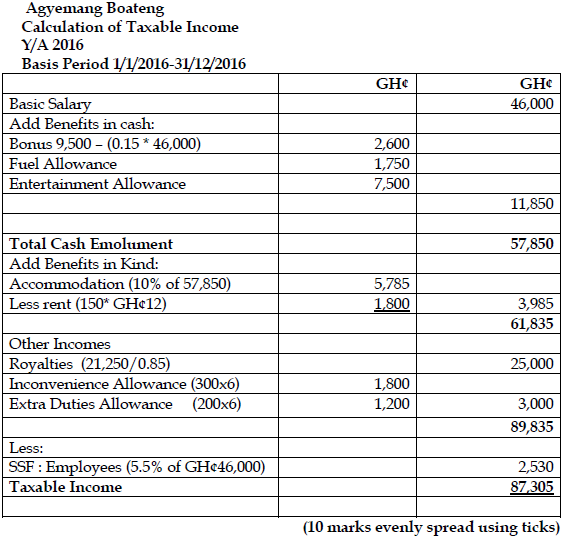

Agyemang’s earnings and entitlements from ICL for the year of assessment ended 31 December 2016 is as seen below:

. GH¢

Basic Salary 46,000

Bonus 9,500

Fuel allowance 1,750

Entertainment allowance 7,500

Additional information:

- Agyemang stays in a fully furnished ICL bungalow at East Legon in Accra. ICL charges him a rent of GH¢150 per month.

- Agyemang makes use of ICL’s company vehicle, driver and fuel for official use only.

- On 1 January 2016, Agyemang successfully applied for a GH¢10,000 loan from his employer, ICL. His employer charged him interest of 2% per annum on the loan. During this period, Bank of Ghana policy rate was 15%. The loan was repayable within ten months.

- On 1 October 2016, Agyemang commenced part-time lecturing in Accounting at a local private Senior High School. He was paid monthly for his services and the total amount received for the three months ended 31 December 2016 was GH¢5,000 gross.

Agyemang’s other non-employment related income received during the year ended 31 December 2016 were:

. GH¢

Net royalties received for his Accounting text book 21,250

Gross local company dividends (Unquoted Company shares) 13,000

Interest on Bank deposits from local financial institutions 10,000

Gross lottery winnings 12,000

Required:

i) Calculate Agyemang’s taxable income for the year ended 31 December 2016. (10 marks)

View Solution

ii) State AMA’s tax obligation when making the disbursement of GH¢10,000 to ICL. (1 mark)

View Solution

In the absence of any further details on AMA or ICL being exempt from withholding taxes, AMA is required to withhold 7.5% on the engagement and remit same to GRA on or before the 15th of the month following the month of payment.

iii) What are the tax implications to Agyemang with respect to the following: (2 marks)

- Part-time lecturing,

- Royalty,

- Dividends, and

- Interest on bank deposit.

View Solution

- The Part-time teaching would be taxed at 10% which is final and would not be added to Agyemang Boateng’s income.

- The royalty income is taxed at 15% which is on account. This was net and was grossed up and added to the income of Agyemang Boateng.

- The dividend from the local company shares is taxed at 8% which is final.

- The interest income on the bank deposit from a local financial institution is tax exempt.

iv) What is the tax implication of the loan taken by Agyemang? (1 mark)

View Solution

The loan taken by Agyemang Boateng would not be treated as benefit in kind because:

- The Loan repayment period does not exceed 12 months.

- The loan amount of GH¢ 10,000 does not exceed his 3 months basic salary of GH¢46,000/12 * 3 months = GH¢11,500.

b) Section 7(m) of the Income Tax Act, 2015 (Act 896) as amended indicates that ‘the income of an individual from employment in the public service of the government of a foreign country in Ghana is exempt from tax’.

Required:

Identify FOUR (4) conditions for granting such an exemption. (2 marks)

View Solution

The income of an individual from employment in the public service of the government of a foreign country is tax exempt where:

- The individual is either a non-resident or resident in the country solely by reason of performing that employment;

- The individual does not exercise any other employment or carry on business in the country;

- The income is payable from the public funds of the foreign country; and

- The income is subject to tax in foreign country.