May 2017 Q4

Straight-to-Heaven church is planning its annual camp meeting in December 2017. The church has four branches and the annual camp meeting is the first major programme after all the head pastors attended a leadership conference on the theme “Blending faith and Science in Church Decision Making.”

The General overseer of the church wishes to apply the scientific principles learnt at the conference in deciding between two major venues for 2017 annual comp meeting. Hitherto, the general overseer or his wife would veto where annual camp meetings are held. The following information are relevant for the decision.

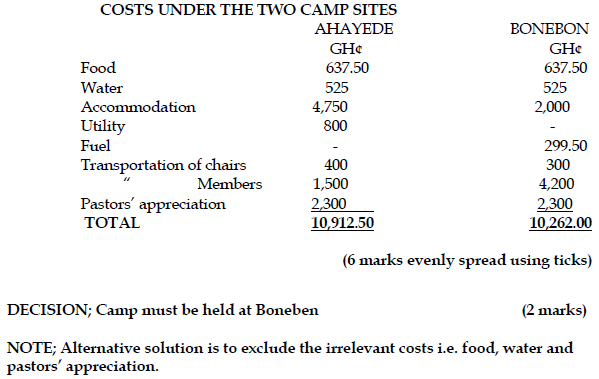

i) Seven pastors will facilitate the Camp meeting. ‘Food 4 All’ restaurant will be assigned the responsibility of providing food for the pastors. They have indicated that a meal for a pastor would cost GH¢5. This cost is expected to increase by one-half if a pastor attends the camp with his wife. All pastors will be fed three times daily but only three pastors plan to attend the conference with their wives. Church members will take care of their own feeding but all camp expenses of pastors will be borne by church members.

ii) Water to be served at the camp meeting. 100bags of sachet water at GH¢2 each and 25 boxes of 750mil bottled water at GH¢13 per box.

iii) The church plans to either have the conference at Ahayede (A) or Bonebon (B) camp sites. Accommodation cost per head per day at Ahayede is GH¢2 for the first 400 participants and GH¢1.5 for any additional participant. Bonebon will not charge any fee but the church will have to show appreciation, which will be in the neighbourhood of GH¢2,000 after the camp.

iv) Ahayede Campsite will require the payment of electricity and water bills of GH¢300 and GH¢500 respectively.

v) It is expected that 96 litres of fuel at GH¢3.12 per litre will be needed at Bonebon campsite.

vi) Transportation cost for chairs and canopies will be GH¢400 if the camp is undertaken at Ahayede and GH¢300 if the camp is sited at Bonebon. Each church member’s transportation cost will be GH¢3 if Ahayede is chosen as the venue but this figure is expected to double if the camp is taken to Bonebon.

vii) Pastors’ appreciation. Apart from the general pastor who will receive GH¢500, each pastor will receive GH¢300 as appreciation support.

viii) The church plans that 700 church members and pastors will take part in the annual camp meeting if it is undertaken at Bonebon while 500 members will attend the camp if it is held at Ahayede even though the two camp sites can each take 1,000 people. The camp will last for 5 days.

Required:

i) Using relevant costing, advise management of the church the site they should hold the annual camp meeting. (8 marks)

View Solution

ii) Suggest TWO qualitative factors that should be considered on deciding on the venue. (4 marks)

View Solution

- Can the venue guarantee proper safety and security of participants?

- Is there any competing events in the venue for the days for which the camp meeting is planned?

- Is the church having a contingency plan in the event of poor weather?

- Proximity of venue to participants and how it will encourage attendance.

iii) Explain the term sunk costs and identify THREE examples of sunk costs. (3 marks)

View Solution

A sunk cost is a cost that has already been incurred and thus cannot be recovered. A sunk cost differs from future costs that a business may face, such as decisions about inventory purchase costs or product pricing. Sunk costs (past costs) are excluded from future business decisions, because the cost will be the same regardless of the outcome of a decision.

Here are some examples of sunk costs:

- Marketing study: A company spends GH¢50,000 on a marketing study to see if its new product will succeed in the marketplace. The study concludes that the product will not be profitable. At this point, the GH¢50,000 is a sunk cost. The company should not continue with further investments in the product, despite the size of the earlier investment.

- Research and development: A company invests GH¢2,000,000 over several years to develop a left-handed smoke shifter. Once created, the market is indifferent, and buys no units. The GH¢2,000,000 development cost is a sunk cost, and so should not be considered in any decision to continue or terminate the product.

- Training: A company spends GH¢20,000 to train its sales staff in the use of new tablet computers, which they will use to take customer orders. The computers prove to be unreliable, and the sales manager wants to discontinue their use. The training is a sunk cost, and so should not be considered in any decision regarding the computers.

- Hiring bonus: A company pays a new recruit GH¢10,000 to join the organization. If the person proves to be unreliable, the GH¢10,000 payment should be considered a sunk cost when deciding whether the individual’s employment should be terminated. (Any 3 points)