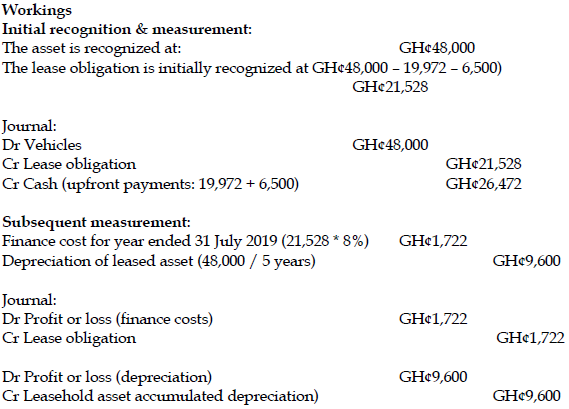

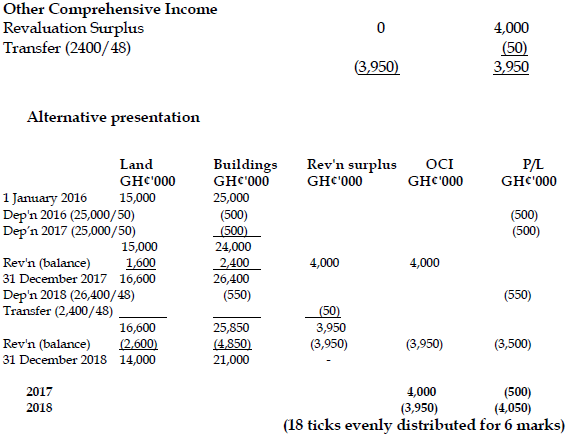

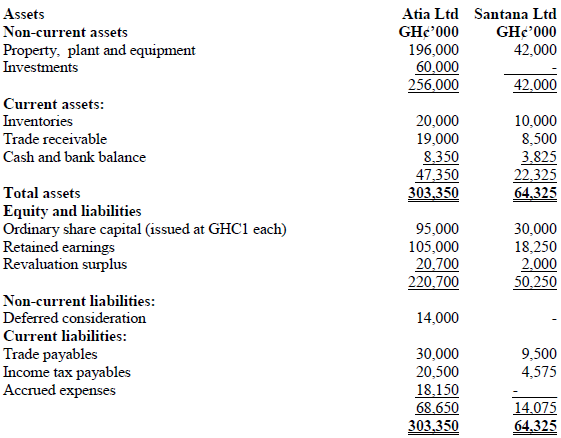

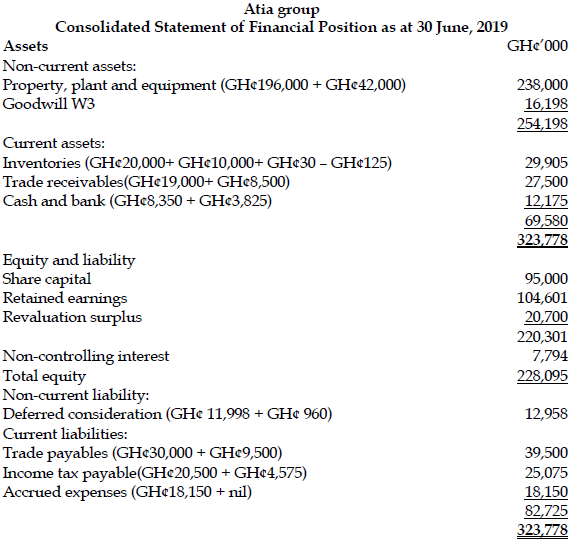

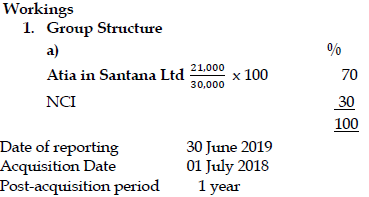

Nov 2019 Q2 d.

Nabdam Ltd (Nabdam) operates in the media and publications industry and reports under IFRS. The 2018 financial statements of Nabdam are still in draft form. The audit is ongoing, and the company intends to authorise the financial statements in April 2019.

Nabdam rents a distribution warehouse in Korle, located beside the River Odorna. On 3 January 2019, the River Odorna burst its banks and GH¢650,000 of Nabdam’s inventory was destroyed by the flood. The inventory was not insured and Nabdam will not receive any compensation for the loss. The company is not sure how to account for this event. The destroyed inventory is included in the inventory figure that is disclosed on Nabdam’s draft statement of financial position at 31 December 2018.

Required:

Explain with justification, the appropriate accounting treatment of the above transaction. (4 marks)

View Solution

- IAS 10 (Events after the Reporting Period) is the applicable accounting standard. IAS 10 outlines that an “event after the reporting period” is an event which occurs between the end of the reporting period and the date that the financial statements are approved.

- The standard differentiates between adjusting and non-adjusting events. Adjusting events provide further evidence on a condition that existed at the reporting date. Adjusting events must be adjusted in the financial statements.

- Non-adjusting events are events that are indicative of conditions that arose after the reporting date. No adjustments are made for non-adjusting events. The flood occurred on the 3rd January 2019. The condition (the flood and damage to the inventory) did not exist at the reporting date of 31st December 2018. Therefore, the event is a non-adjusting event and Nabdam does not have to adjust the 2018 financial statements for the GH¢650,000 inventory loss.

- However, IAS 10, states that if the event is material then the reporting entity must disclose the nature of the event and an estimate of its financial effect. Therefore, as the inventory loss is material, Nabdam would have to make a disclosure describing the nature of the event (a flood affecting a distribution warehouse) and an estimate of the financial effect of the event (GH¢650,000 damage to inventory) in its 2018 financial statements.

*Identification of IAS 10 – 1 mark

*Explanation of the treatment in IAS 10 – 1 mark

*Treatment of as a non-adjusting event – 1 mark

*Disclosure of the nature and effect in the financial statement – 1 mark