May 2020 Q3 a(i)

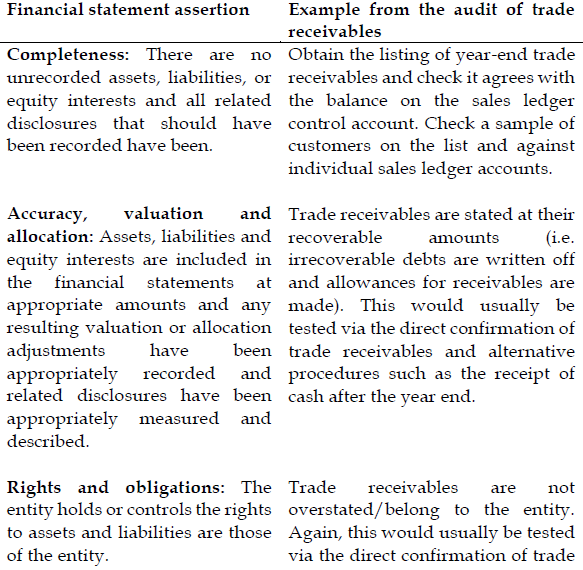

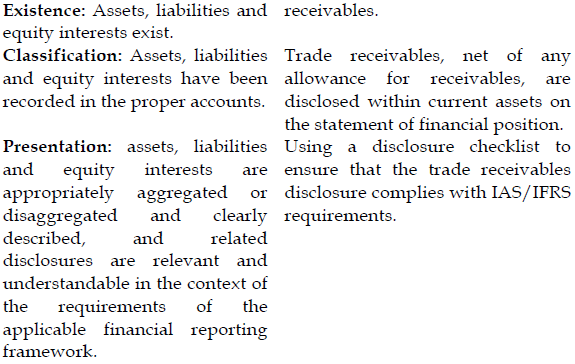

ISA: 500 Audit evidence requires the auditor to obtain sufficient, appropriate evidence to be able to draw reasonable conclusions on which to base the audit opinion. That evidence should be relevant to the financial statements assertions.

Required:

i) Explain the main assertions about account balances and provide an example of each one by reference to the audit of trade receivables. (8 marks)

View Solution