MOBILE MONEY SERVICE

Introduction

The government of Ghana has been concerned with low savings culture, low financial inclusion as well as high cash-based transactions in the country. In the year 2005, the government decided to pursue policies to grow the financial services industry (FSI) since it was indispensable to the accelerated economic growth required to make the country middle income country. The key service providers include banks, non-bank institutions, and mobile network operators (MNOs). By the close of 2017, 52% of the population would remained excluded from any form of financial services

There is generally high cost of credit in the country as the banks complain of difficulty in mobilizing deposits. Ghana is said to have one of the highest lending rates to the world, placing second in the latest ranking released by Trading Economics, a development which has been identified as a disincentive for the business community. The government budget deficit as a percentage of Domestic Product (GDP) decreased from 8.7% in 2010 to 8.5% in 2016 respectively. In the past, the government relied on external capital markets to fund the budget deficits but, following the worsening deficit figures, international financial organisations have raised concerns about the need for the government to ensure fiscal discipline.

The major development that revolutionized the FSI was the launch of mobile money solution in 2009 by the four MNOs. Mobile money rides on the backbone of the mobile telephony infrastructure of the mobile networks operators. This allows mobile money to be operated from wherever there is network coverage. It is estimated that there is 65% mobile network coverage in Ghana.

The MNOs deliver mobile financial services largely through thousands of registered mobile money agents throughout the country. This effectively makes agents closer to the customers than traditional banks and non-bank financial institutions. Most of the traditional banks’ branch networks are concentrated in the urban centres to the exclusion of peri-urban and rural communities. The combination of these two factors enables mobile money services to be administered quickly and efficiently, and in the most remote areas. The capital requirement for registration as mobile money agent is GH¢4,000 and the daily transaction limit is currently at GH¢5,000. On the average, agents operate one network mobile money, while very few agents have signed up to two or more different mobile money solutions. The total number of agents have increased from about 17,467 in 2013 to 93,376 as at close of 2016, and National Communication Authority (NCA) has projected rapid annual growth for the next three years (2017-2019).

The Environment

Mobile money started in the country largely with two products – airtime purchases and domestic remittances for small amounts. With the passage of time, mobile money service offerings have expanded to include bill payments, Point of Sales (POS) payments, fund transfers in increasingly larger amounts, and deposit collection by banks and non-bank financial institutions. The

expansion of the product offerings from mobile money makes it more appealing to a broad spectrum of mobile subscribers in the country. Customers are, therefore, keeping larger amounts in their wallets than they used to, and are using the expanding offerings from mobile money at the expense of existing products from the banks. There is growing mobile phone penetration rate as increasing number of mobile phone users are subscribing to more than one mobile network.

Furthermore, mobile money has become very popular among middle and lower income earners who make up about 80% of the population. The operation of mobile money on the handset is very easy and convenient and can be done from the comfort of one’s location. All that prospective mobile money customers require are a registered SIM card on the network of choice and a valid national ID. With these they can be set up and ready to use their mobile wallets within minutes. The processes for setting up and using bank accounts are however more complex due to stricter Know Your Customer (KYC) requirement by the Central Bank. Remittances through mobile money is instant at a fee of 1% of amount remitted or received. Mobile money transactions in Ghana reached GH¢679.17 million by the end of June 2016, according to the Bank of Ghana’s Payment Systems Department and it is expected to hit GH¢35 billion by the close of 2017. Until very recently, the income from mobile money was not taxed but the Minister of Finance in his 2017 mid-year review hinted of plans to impose a tax on the fees from mobile money operations.

The mobile money operations face the issue of network instability and system downtime as mobile network operators have not correspondingly expanded their infrastructure to match the growing subscribers. Sometimes, the agents are unable to meet cash demands of the customers due to mismatch in net remittances. This is more pervasive in the rural communities. Due to the weaknesses inherent in the issuance of valid Identity Cards (IDs), there are many fake ID cards and this has resulted in fraudsters having a field day. Some agents and customers have lost sums of money to fraudsters.

The customers and other players in the FSI have expressed concerns about their inability to carry out mobile money services across the various networks. Accordingly, the Central Bank has tasked its Payment Systems Department to ensure interoperability of mobile money across all networks in the country by June 2018. The government believes that mobile interoperability will deepen financial inclusion.

Regulation

Mobile money services it has operated without any regulatory framework. The industry players, according to a recent survey, suggested that the long-term survival of the mobile money service require stringent regulation. The Central Bank has now published guidelines for mobile money operators to be licensed as Dedicated Electronic Money Issuers (DEMI). The provisions include stringent KYC on the agents before registration, monthly returns on the activities of the agents, prosecution of the agents for mobile money fraud, etc. The mobile network operators are required to pay interest at the rate of 6% p.a. on the float on the mobile wallet.

Proposal

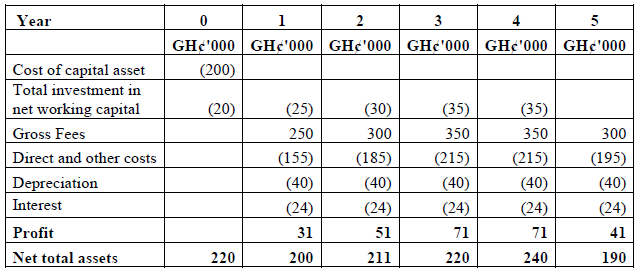

The Board of Directors of Excellent Telephone Service Ltd at a recent meeting discussed the possibility of opening a new unit to provide mobile money service to take advantage of the newly regulated industry. The Finance Director has presented a five-year estimates for the new venture as:

For taxation purposes, capital allowances will be available against the taxable profits of the venture, at 25% per annum on a reducing balance basis and in year 5 any balance would be granted as additional capital allowance. The rate of tax on taxable profits is 25% and tax is paid one year in arrears. The capital assets will have a zero-salvage value at the end of 5 years. The after-tax weighted average cost of capital is estimated to be 24% per anum.

Required:

Analyse the competitive environment of mobile money segment using Porter’s Five Forces. (10 marks)

View Solution

Threat of New Entrant

- Capital requirement – the minimum capital required by an agent is GH¢4,000 which appears to be reasonably within the reach of average Ghanaian. This may be deduced from the number of people joining as agent rising from 17,467 in 2013 to 93,376 in 2016 and projected annual rapid growth in the next 3 years.

- New Legislation and KYC requirements – with introduction of new legislation and KYC requirements, some people who may have questionable record may not be allowed to operate mobile money. But this may not constitute serious entry barrier since once a person does not have any criminal record he/she can pass the KYC test.

- Switching cost– since the mobile money appears to be standardised service and not differentiated it will not cost customers anything to switch from one agent to another hence new agents can always attract customers and will not constitute any significant entry barrier.

From the above analyses entry barriers are generally low and this will make competition much keener as more new agents join the fray.

Rivalry among existing agents - Number of agents – there are large number of agents and the number is increasing and therefore competition for customers is going to be very intense all things being equal.

- Sector/industry growth rate – the mobile money service looks to be in growth stage. Given the number of agents joining the business one can assert that the segment is yet not at maturity or declining stage. With the potential for growth competition is likely not to be intense as compared to maturity or declining stage.

- Pending implementation of mobile interoperability – successful implementation of intended mobile interoperability which will allow transactions across all the four networks, this is likely to intensify the competition among the agents.

- Standard nature of service – the mobile money service is not differentiated in any way among the various networks. The fees charge is the same across the four networks hence this is likely to intensify competition since a customer can walk to any nearest point and get the service.

- Low switching cost – due to low switching cost there will be intense rivalry among mobile money providers.

Bargaining Power of Customers/Buyers - Self-service – the customers are able to do a number of mobile transactions by themselves including airtime purchase, transfer from one mobile wallet to another, pay utility bills etc. The only point that mobile money agents are most needed is where a customer wants to either put money on his or her wallet or physically withdraw from the wallet. This makes customers somehow power and effectively deny agents some fees.

- Low switching costs – the customers really are not facing any switching costs hence mobile agents are at their mercy and can chose to transact business with any agent at any place of convenience. Perhaps to have repeated business the agents would have to do extra work to encourage customers to always return to them for business. This makes customers very powerful.

- Access to many agents – the number of agents are increasing and it is projected to further increase. The gives the customer many alternatives and that makes the customer bargaining power very strong.

Bargaining power of suppliers - Concentrated or Dominant or Few Suppliers – the main suppliers to the agents are the four network providers. These operators are large and can dictate the terms of the relationship. The agents are very small relative to the network operators. Again, most of the fees end up with the operators. Hence the operators are very powerful.

- There are no alternatives/substitutes – the mobile money service was launched and is being operated by mobile network operators and are leveraging on their existing nation-wide infrastructure. There are no other companies that have nation-wide capability to deliver mobile money solution apart from the four network operators. This even makes the bargaining power of network operators very potent and veritable.

- The agent group is not an important customer of the network operators group – the network operators core business is voice and data which make up the substantial source of revenue. Mobile money service is just ancillary to their main lines of business. This makes the bargaining power of suppliers still very strong.

Threat of substitute products - Less attractive substitute services from banks – given less stringent KYC requirements of mobile money compared to higher KYC requirements, convenience of mobile money compared to the banks, increasingly mobile money services are more attractive. This make bank services as substitute less of a threat to mobile money.

- Low/zero switching cost for customers – it does not cost customer to switch to mobile money for remittances and other transactions executable on the mobile money solution. This again makes banking services as substitute no threat to mobile money.