You are the Financial Controller of Oxtom Ltd. Pep Ltd is a competitor in the same industry and it has been operating for 20 years. Summaries of Pep Ltd’s Statements of Profit or Loss and Financial Position for the previous three years are given below.

Required:

Write a report to the Chief Executive Officer of Oxtom Ltd,

a) Analysing the performance of Pep Ltd and showing any calculations in an appendix to this report. (14 marks)

View Solution

To : Chief Executive Officer

From : Financial Controller

Subject : Performance Analysis of Water Limited from 2016 to 2018

Date : 4th November 2019

Introduction

This performance report relates to the financial statements of Water Limited for the period 2016 to 2018. The report covers the profitability, operating efficiency, liquidity and solvency positions of Water Limited over the period under review. An appendix is attached to this report which shows the ratios calculated as part of the performance review.

Profitability

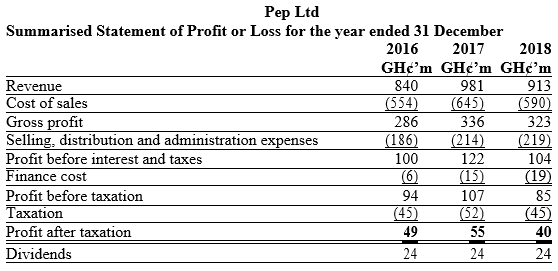

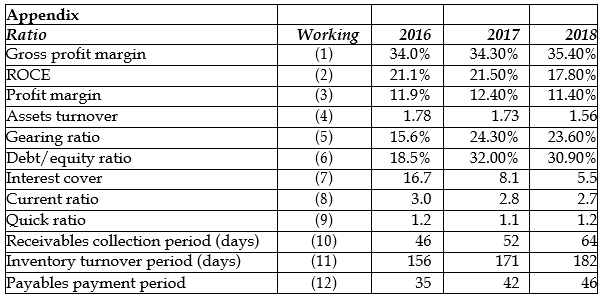

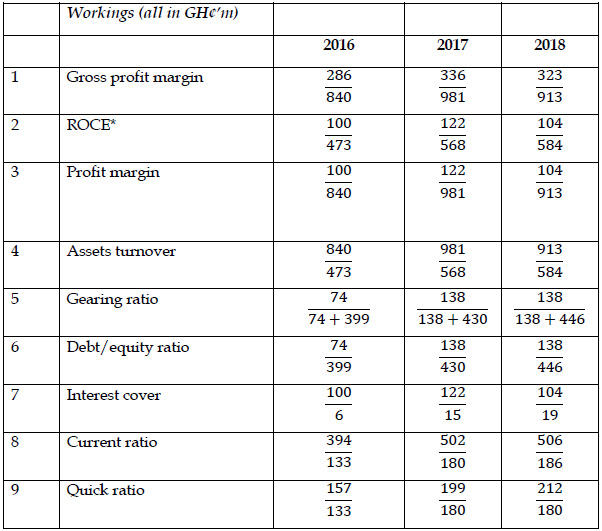

The gross profit margin has remained relatively static over the three year period, although it has risen by approximately 1% in 2018. ROCE, while improving very slightly in 2017 to 21.5% has dropped dramatically in 2018 to 17.8%. The net profit margin has also fallen in 2018, in spite of the improvement in the gross profit margin. This marks a rise in expenses which suggests that they are not being well controlled. The utilization of assets compared to the turnover generated has also declined reflecting the drop in trading activity between 2017 and 2018.

Operating Efficiency

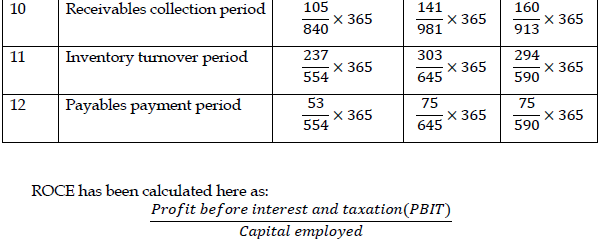

It is apparent that there was a dramatic increase in trading activity between 2017 and 2018, but then a significant fall in 2018. Revenue rose by 17% in 2017 but fell by 7% in 2018. The reasons for this fluctuation are unclear. It may be the effect of some kind of one-off event, or it may be the effect of a change in product mix. Whatever the reason, it appears that improved credit terms granted to customers (receivables payment period up from 46 to 64 days) has not stopped the drop in sales.

Liquidity

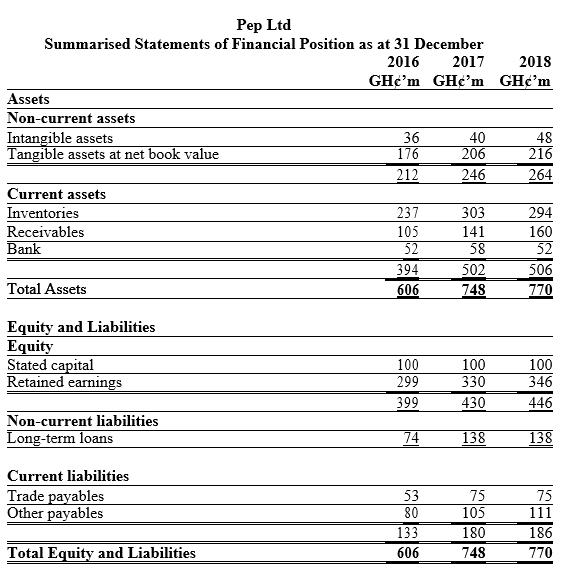

Both the current ratio and quick ratio demonstrate an adequate working capital situation, although the quick ratio has shown a slight decline. There has been an increased investment over the period in inventories and receivables which has been only partly financed by longer payment periods to trade payables and a rise in other payables (mainly between 2016 and 2017).

Solvency/Gearing

The level of gearing of the company increased when a further GH¢64m was raised in long-term loans in 2017 to add to the GH¢74m already in the statement of financial position. Although this does not seem to be a particularly high level of gearing, the debt/equity ratio did rise from 18.5% to 32.0% in 2017. The interest charge has risen to GH¢19m from GH¢6m in 2016. The 2017 charge was GH¢15m, suggesting that either the interest rate on the loan is flexible, or that the full interest charge was not incurred in 2017. The new long-term loan appears to have funded the expansion in both fixed and current assets in 2017.

Where capital employed = shareholders’ funds plus payables falling due after one year and any long-term provision for liabilities and charges. It is possible to calculate ROCE using net profit after taxation and interest, but this admits variations and distortions into the ratios which are not affected by operational activity.

2 marks for the structure of the report = 2 marks

2 marks for analysis of performance x 4 areas covered = 8 marks

4 marks for Appendix (12 ratios computed: 4 ratios x 3 years) = 4 marks

b) Summarising THREE (3) areas which require further investigation, including reference to other pieces of information which would complement your analysis of the performance of Pep Ltd. (6 marks)

View Solution

Areas for further investigation include the following;

i) Long-term loan: There is no indication as to why this loan was raised and how it was used to finance the business. Further details are needed of interest rate(s), security given and repayment dates.

ii) Trading activity: The level of sales has fluctuated in quite a strange way and this requires further investigation and explanation. Factors to consider would include pricing policies, product mix, market share and any unique occurrence which would affect sales.

iii) Further analysis: It would be useful to break down some of the information in the financial statements, perhaps into a management accounting format. Examples would include the following.

** Sales by segment, market or geographical area

** Cost of sales split, into raw materials, labour and overheads

** Inventory broken down into raw materials, work in progress and finished goods

** Expenses analysed between administrative expenses, sales and distribution costs.

iv) Accounting policies: Accounting policies may have a significant effect on certain items. In particular, it would be useful to know what the accounting policies are in relation to intangible assets (and what these assets consist of), and whether there has been any change in accounting policies.

v) Dividend policy: Water Limited has maintained the level of dividend paid to shareholders during the three year period. Presumably, Water Limited would have been able to reduce the amount of long-term debt taken on if it had retained part or all of the dividend during this period. It would be interesting to examine the share price movement during the period and calculate the dividend cover. (3 areas well explained and related to the question @ 2 marks: 6 marks)