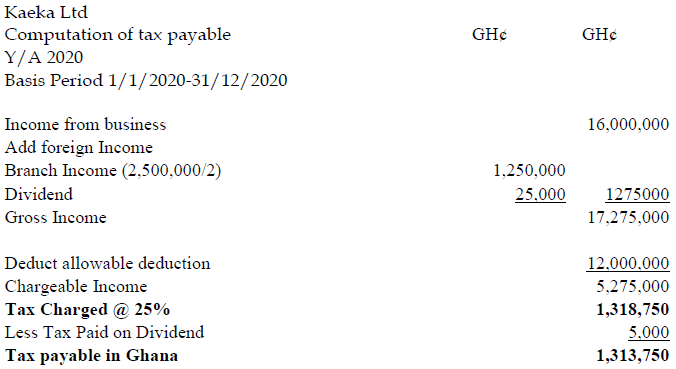

Kaeka Ltd is a resident company providing cleaning services in Ghana. For the first time in the history of the entity, it launched operations as an external company in January 2020 in Lusaka- Zambia. It came to light that the entity earned the equivalent of GH¢2,500,000, which was evenly made for the 2020 year of assessment.

On the home front, it earned GH¢16,000,000 in 2020 year of assessment as income in Ghana. Assume that allowable cost of GH¢12,000,000 was incurred. It received a dividend net of tax from a company in Israel it acquired shares from amounting to GH¢20,000 in December 2020. Tax of GH¢5,000 was paid on the dividend received.

Required:

i) Compute the tax payable by Kaeka Ltd. (4 marks)

View Solution

Explanation

Income received from foreign country losses its character hence the dividend added to the income and tax paid in a foreign country given as credit.

Additionally, the branch of the entity in Ghana has become a foreign PE and therefore, its income for the first 183 days is taxable in Ghana. After that, it is exempt from tax.

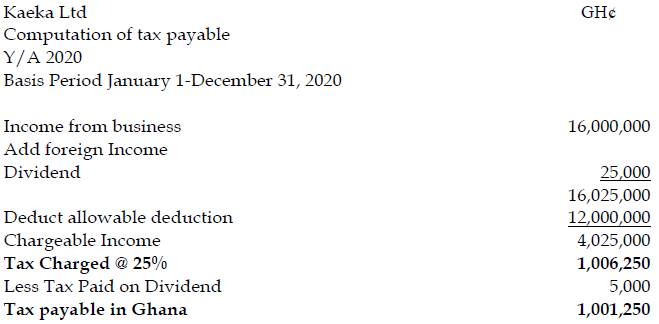

ii) Explain the tax implication if the company made the income from Zambia in the last quarter of 2020. (4 marks)

View Solution

Explanation

Since the foreign Permanent Establishment did not earn the income in the first 183 days or first 6 months, the income shall be exempt from tax in Ghana in line with section 111 of Act 896 (Act 2015).