You are a manager in Sustainability Ghana, an independent member of Sustainability International, a global firm of Chartered Certified Accountants. You are responsible for evaluating proposed engagements and for recommending to a team of partners whether or not an engagement should be accepted by your firm.

EnvironmentalCare Ghana, a listed company, is an existing audit client and is an international energy producing company, with a global network including 220 countries and 300,000 employees. The company offers electricity using renewable resources to individual and corporate customers, as well as storage and logistical services.

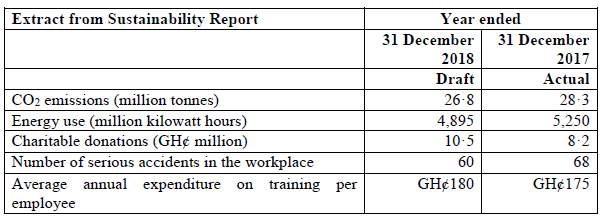

EnvironmentalCare Ghana takes its corporate social responsibility seriously, and publishes social and environmental key performance indicators (KPIs) in a Sustainability Report, which is published with the financial statements in the annual report. Partly in response to requests from shareholders and pressure groups, EnvironmentalCare Ghana’s management has decided that in the forthcoming annual report, the KPIs should be accompanied by an independent assurance report. An approach has been made to your firm to provide this report in addition to the audit.

To help in your evaluation of this potential engagement, you have been given an extract from the draft Sustainability Report, containing some of the KPIs published by EnvironmentalCare Ghana. In total, 25 environmental KPIs, and 50 social KPIs are disclosed.

You have also had a meeting with Kofi Ghana, the manager responsible for the audit of EnvironmentalCare Ghana, and notes of the meeting are given below.

Notes from meeting with audit manager, Kofi Ghana

Sustainability Ghana has audited EnvironmentalCare Ghana for three years, and it is a major audit client of the firm, due to its global presence and recent listing on two major stock exchanges. The audit is managed from the Airport office, which is also the location of the global headquarters of EnvironmentalCare Ghana. The audit work is nearly complete, and the annual report is to be published in about four weeks, in time for the company’s meeting, scheduled for 31 January 2019.

No work has been done on the KPIs, other than review them for consistency, as we would with any ‘other information’ issued with the financial statements. The KPIs are produced by EnvironmentalCare Ghana’s Sustainability Department, located in Fartown. There has been no visit to EnvironmentalCare Ghana’s offices in Fartown as it is in a remote location overseas, and the departments based there are not relevant to the audit.

Audit procedures were performed on the charitable donations, as disclosed in a note to the financial statements, and our evidence indicates that there have been donations of GH¢9 million this year, which is the amount disclosed in the note. However, the draft KPI has a different figure of GH¢10·5 million, and this is the figure highlighted in the draft Chairman’s Statement as well as the draft Sustainability Report. GH¢9 million is material to the financial statements.

Your firm has recently established a sustainability reporting assurance team based at the Airport office and if the engagement to report on the Sustainability Report is accepted, it would be performed by members of that team, who would not be involved with the audit.

Required:

b) Recommend procedures that could be used to verify the following draft KPIs:

i) The number of serious accidents in the workplace; and (3 marks)

View Solution

- Procedures to verify the number of serious accidents in the workplace

- Review records held by human resources, which summarise the number and type of accidents reported in the workplace.

- Review the accident log book from a sample of locations.

- Discuss the definition of a ‘serious’ accident (as opposed to a ‘minor’ accident) and establish the nature of criteria applied to an accident to determine whether it is serious.

- Review correspondence with legal advisors which may indicate legal action being taken against EnvironmentalCare Ghana in respect of serious accidents in the workplace.

- Review minutes of board meetings for discussions of any serious accidents and associated repercussions for the company.

- Ascertain through discussion with management and/or legal advisors, if EnvironmentalCare Ghana has any convictions for health and safety offences during the year (which could indicate that serious accidents have occurred).

- Enquire as to whether the company has received any health and safety visits (the regulatory authority would usually perform one if an employee has a serious accident). Review documentation from any health and safety visits for evidence of any serious accidents.

- Consider talking to employees to identify if any accidents have not been recorded in the accident book.

(Any 3 points @ 1 mark each = 3 marks)

ii) The average annual expenditure on training per employee. (3 marks)

View Solution

Procedures to verify the annual training spend per employee

- Review EnvironmentalCare Ghana’s approved training budget in comparison to previous years to ascertain the overall level of planned spending on training.

- Obtain a breakdown of the total training spend and review for any items mis-classified as training costs.

- Agree significant components of the total training spend to supporting documentation such as contracts with training providers and to invoices received from those providers.

- Agree the total amount spent on significant training programmes to cash book and/or bank statements.

- Using data on total number of employees provided by the payroll department, recalculate the annual training spend per employee. (Any 3 points @ 1 mark each = 3 marks)