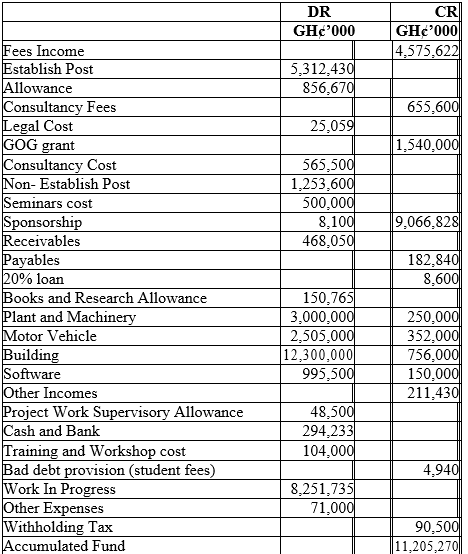

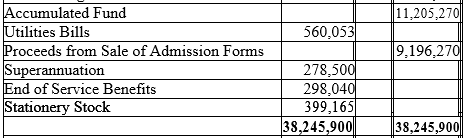

The following Trial Balance relates to Bunsu Education College, a public tertiary educational institution in Ghana, as at 31/12/2018.

Additional information:

i) The college has adopted the accrual basis International Public Sector Accounting Standards (IPSAS) as the basis for the preparation of its financial statements.

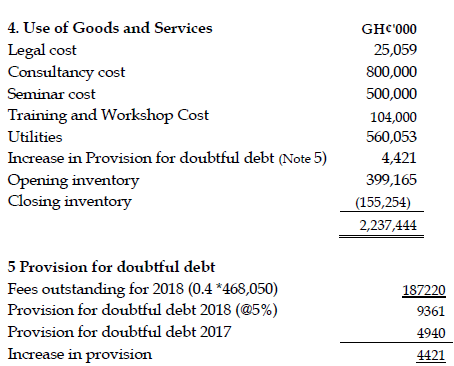

ii) Stationery stock as at 31/12/2018 was GH¢200,500,000 but have a Net Realisable Value of GH¢ 155,254,000

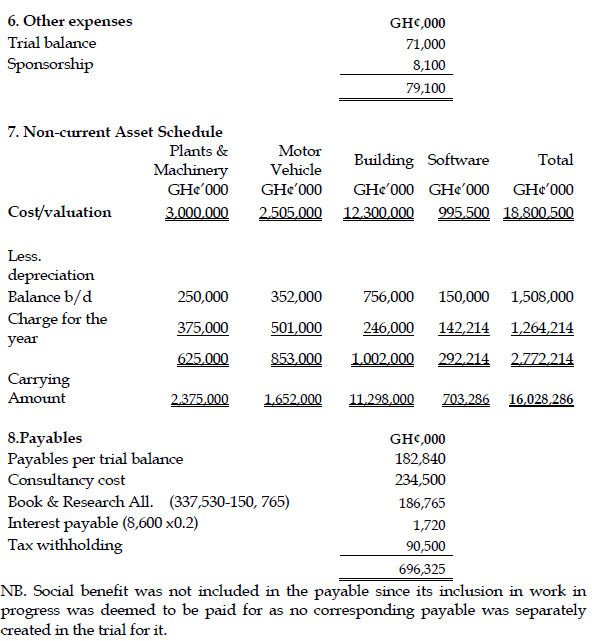

iii) Social benefits of GH¢1,720,000 yet to be paid during the year was included in the Work In Progress value. Consultancy cost amounting to GH¢234,500,000 was incurred but not yet paid.

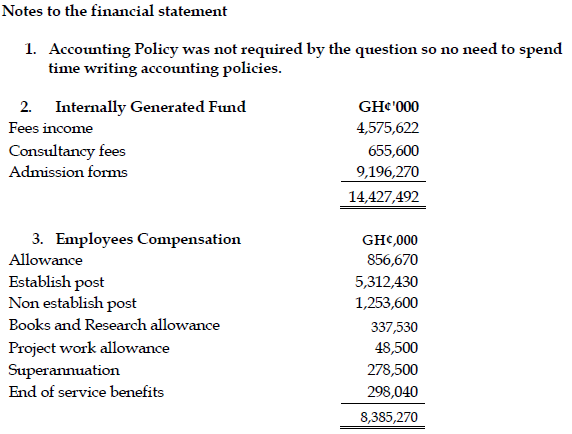

iv) Books and Research Allowance was received from Government during the period amounting to GH¢337,530,000 for disbursement to qualified Lecturers and Administrative staff.

v) Provision is to be made for interest on loans.

vi) 60% of the receivables represent an amount of students’ fees outstanding as at 31/12/2017. Provision for doubtful debt is estimated to be 5% of outstanding school fees.

vii) The university uses straight line basis of depreciation for Capital Assets. Capital Assets and their useful lives are detailed out below:

Assets Useful Life

Plant and Machinery 8 years

Motor Vehicle 5 years

Building 50 years

Software 7 years

Required:

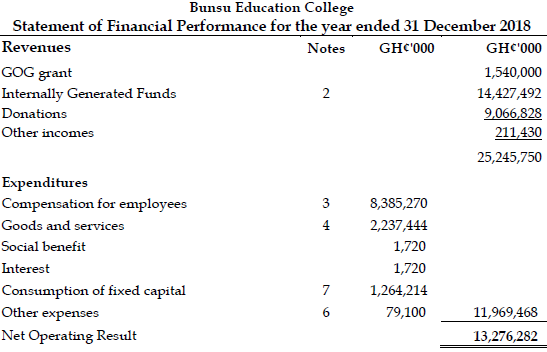

i) Prepare a Statement of Financial Performance for Bunsu Educational College for the year ended 31/12/2018. (8 marks)

View Solution

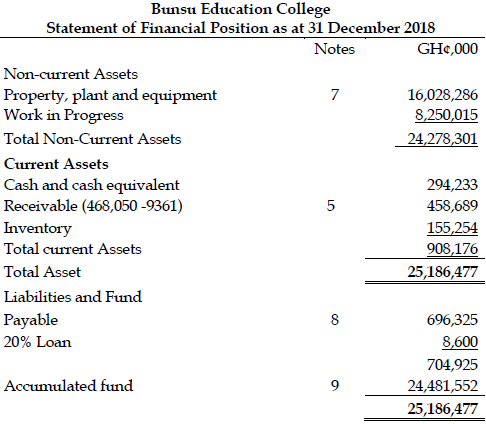

ii) Prepare a Statement of Financial Position as at 31/12/2018. (6 marks)

View Solution

View All Workings