A colleague has been taken ill. Your managing director has asked you to take over from the colleague and to provide urgently-needed estimates of the discount rate to be used in appraising a large new capital investment. You have been given your colleague’s working notes, which you believe to be numerically accurate.

Working notes: Estimates for the next five years (annual averages)

Stock market total return on equity 16%

Own company dividend yield 7%

Own company share price rise 14%

Standard deviation of total stock market return on equity 10%

Systematic risk of own company return on equity 14%

Growth rate of own company earnings 12%

Growth rate of own company dividends 11%

Growth rate of own company sales 13%

Treasury bill yield 12%

The company’s gearing level (by market values) is 1 : 2 debt to equity, and after-tax earnings available to ordinary shareholders in the most recent year were GH¢54,000,000, of which GH¢21,400,000 was distributed as ordinary dividends.

The company has 1 million issued ordinary shares which are currently trading on the Stock Exchange at GH¢3.21. Corporate debt may be assumed to be risk-free. The company pays tax at 30% and personal taxation may be ignored.

Required:

Estimate the company’s weighted average cost of capital using: (10 marks)

State clearly any assumptions that you make.

Under what circumstances these models would be expected to produce similar values for the weighted average cost of capital?

i) The dividend valuation model;

View Solution

If we assume a constant growth in dividends, we may estimate the cost of equity by using:

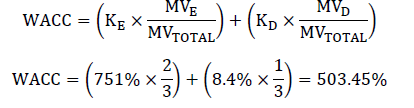

Cost of debt (Kd), as corporate debt is assumed to be risk free, is 12%, the Treasury bill yield.

The after-tax cost is 12(1 – 0.30) = 8.4%

The weighted average cost of capital (WACC) is found as follows:

ii) The capital asset pricing model.

View Solution

Cost of equity may be estimated using:

![]()

The beta value of the security may be found using:

![]()

![]()

If the stock market is in equilibrium, and the inputs into the models are correctly specified (e.g., the dividend valuation model reflects only systematic risk), then the cost of equity Ke from the dividend valuation model should approximately equal the expected return on equity E(re) of the CAPM.