a) According to the Conceptual Framework for General Purpose Financial Reporting (GPFR) for Public Sector Entities issued by IPSASB, GPFR of public sector entities are developed primarily to respond to the information needs of the primary users who do not possess the authority to require a public sector entity to disclose the information they need for accountability and decision-making purposes. It adds that the objectives of financial reporting are therefore determined by reference to the users of GPFRs, and their information needs.

Required:

i) In relation to the Conceptual Framework, which category of users is regarded as primary users of the GPFRs of public sector entities? (2 marks)

View Solution

Primary users of GPFRs are service recipients and their representatives and resource providers and their representatives.

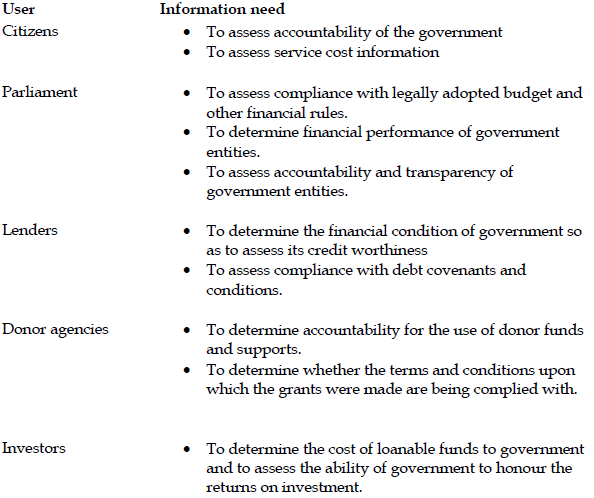

ii) When preparing financial reports for the Consolidated Fund of Government, identify THREE (3) primary users and their information needs you would endeavour to meet. (3 marks)

View Solution

b) Public sector entities have downplayed the role of quality financial reporting in public financial management. In recent times, the government has been encouraged by its developing partners to ensure effective financial management and reporting in the public sector by investing in people and processes. The developing partners have touted financial reporting as a major solution to public financial management requirements of developing countries.

Required:

Explain FOUR (4) objectives of financial reporting in public financial management. (4 marks)

View Solution

- To provide financial information useful for determining and predicting the flows, balance and requirements of short-term financial resources of government;

- To provide financial information useful for determining and predicting the economic condition of the government unit and changes therein;

- To provide financial information useful for monitoring performance under terms of legal, contractual and fiduciary requirements;

- To provide information useful for evaluating managerial and organizational performances;

- Determining the costs of programme, functions and activities in a manner which facilitates analysis and valid comparison, with established criteria among time periods and with other sector ministers;