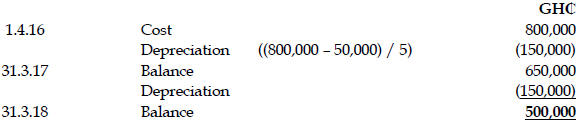

Devine Education Ltd acquired an item of plant at a cost of GH¢800,000 on 1 April 2016. The plant had an estimated residual value of GH¢50,000 and an estimated useful life of five years, neither of which has changed. Devine Education Ltd uses straight-line depreciation.

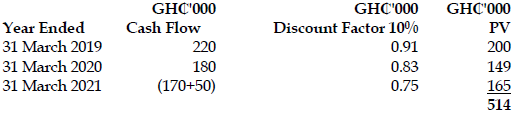

On 31 March 2018, Devine Education Ltd was informed by a major customer (who buys products produced by the plant) that it would no longer be placing orders with Devine Education Ltd. Even before this information was known, Devine Education Ltd had been having difficulty finding work for this plant. It now estimates that net cash inflows earned from the plant for the next three years will be:

Year ended: GH¢’000

31 March 2019 220.00

31 March 2020 180.00

31 March 2021 170.00

Devine Education Ltd has confirmed that there is no market in which to sell the plant as at 31 March 2018, but is confident that it can still be sold for its original estimated realisable value on 31 March 2021. Devine Education Ltd’s cost of capital is 10% and the following values should be used:

Value of GH¢1 at: GH¢

End of year 1 0.91

End of year 2 0.83

End of year 3 0.75

Required:

In line with IAS 36: Impairment of Assets, calculate the carrying amounts of the asset above as at 31 March 2018 after applying any impairment losses. (Note: Calculations should be to the nearest GH¢1,000) (6 marks)

View Solution

Carrying amount of the plant at 31.3.18

As there is currently no market in which to sell the plant, its recoverable amount will be its value in use, calculated as:

As this is greater than the carrying amount, the plant is NOT impaired and will be left at its carrying amount of GH₵500,000.