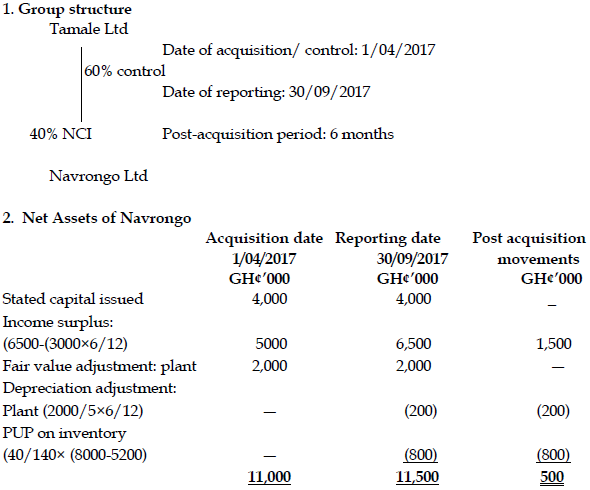

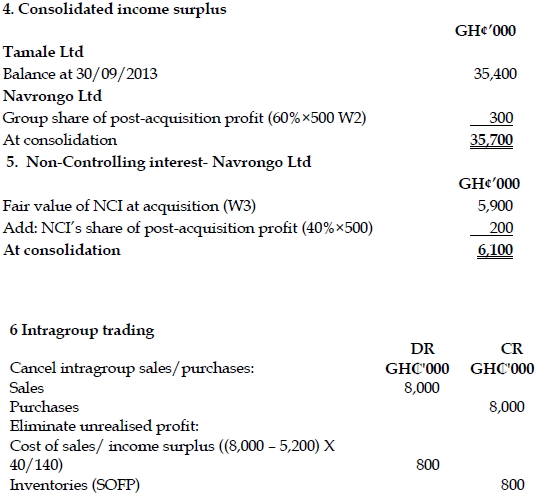

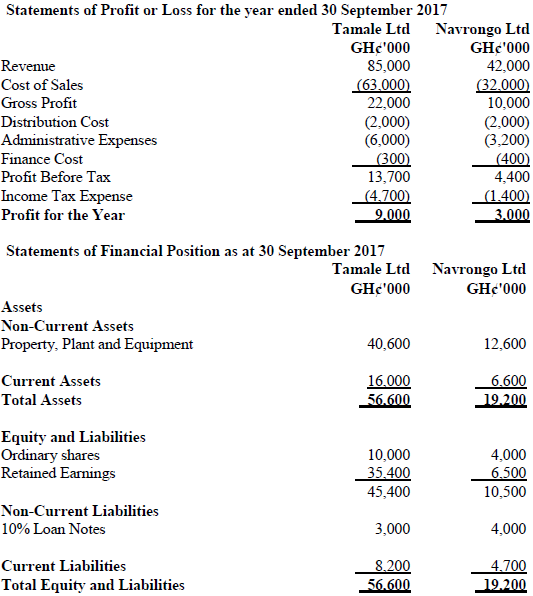

On 1 April 2017, Tamale Ltd acquired 60% of the 4 million ordinary shares of Navrongo Ltd in a share exchange of two shares in Tamale Ltd for three shares in Navrongo Ltd. The issue of shares has not yet been recorded by Tamale Ltd. At the date of acquisition, shares in Tamale Ltd had a market value of GH¢6 each. Below are the summarised draft financial statements of both companies.

The following information is relevant:

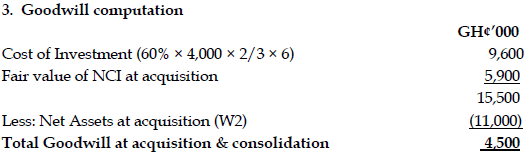

i) At the date of acquisition, the fair values of Navrongo Ltd’s assets were equal to their carrying amounts with the exception of an item of plant, which had a fair value of GH¢2 million in excess of its carrying amount. It had a remaining life of five years at that date (straight-line depreciation is used). Navrongo Ltd has not adjusted the carrying amount of its plant as a result of the fair value exercise.

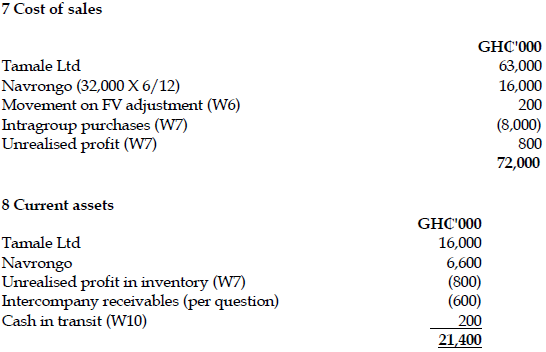

ii) Sales from Navrongo Ltd to Tamale Ltd in the post-acquisition period were GH¢8 million. Navrongo Ltd made a markup on cost of 40% on these sales. Tamale Ltd had sold GH¢5.2 million (at cost) as at 30 September 2017.

iii) Other than where indicated, profit or loss items are deemed to accrue evenly on a time basis.

iv) Navrongo Ltd’s trade receivables at 30 September 2017 include GH¢600,000 due from Tamale Ltd which did not agree with Tamale Ltd’s corresponding trade payable. This was due to cash in transit of GH¢200,000 from Tamale Ltd to Navrongo Ltd. Both companies have positive bank balances.

v) Tamale Ltd has a policy of accounting for any non-controlling interest at fair value. The fair value of the non-controlling interest in Navrongo Ltd at the date of acquisition was estimated to be GH¢5.9 million. Consolidated goodwill was not impaired at 30 September 2017.

Required:

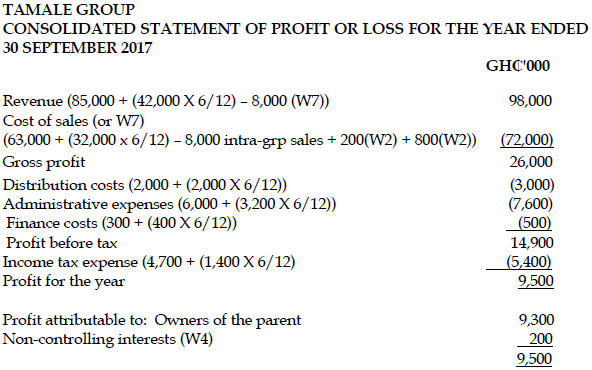

a) Prepare the consolidated statement of profit or loss for Tamale Ltd for the year ended 30 September 2017. (8 marks)

View Solution

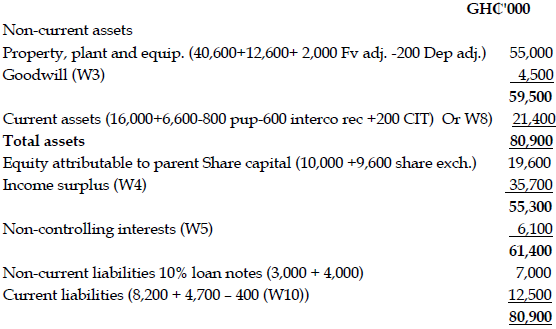

b) Prepare the consolidated statement of financial position for Tamale Ltd as at 30 September 2017. (12 marks)

View Solution

Workings for a & b