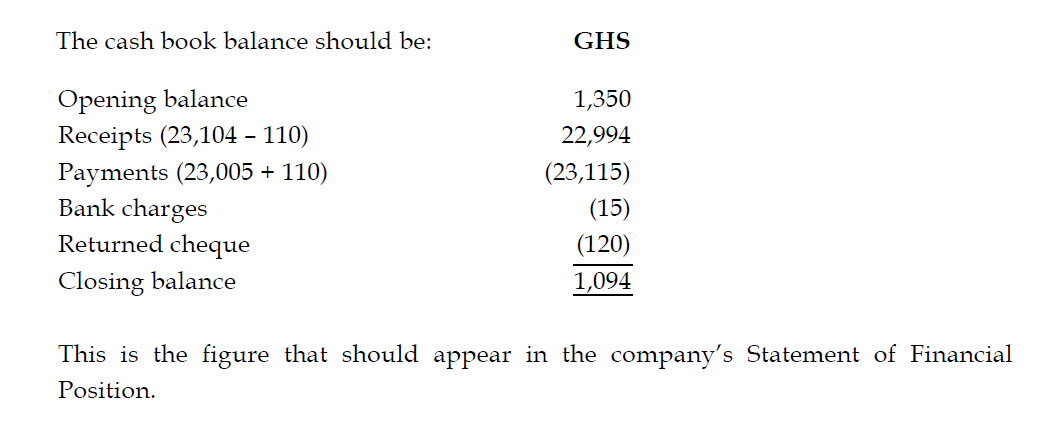

The following is a summary from the cash book of BW Ltd for July 2015:

GH¢

Opening balance 1,530

Receipts 23,104

Payments (23,005)

Closing balance 1,629

On investigation it was discovered that:

i) Bank charges of GH¢15 shown on the bank statement have not been entered in the cash book.

ii) A cheque drawn for GH¢110 to pay a supplier has been entered in the cash book as a receipt.

iii) A cheque from a customer for GH¢120, which was banked (and included above in receipts), has been returned by the bank, but this has not been adjusted in the company’s books.

iv) An error of transposition which occurred in the opening balance of the cash book should have been recorded as GH¢1,350.

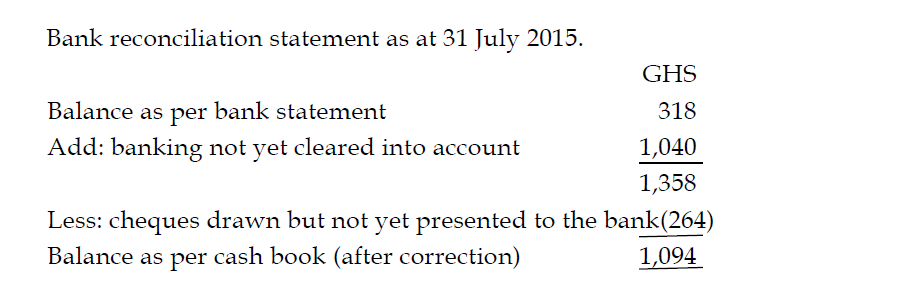

v) Cheques totaling GH¢264 have been sent by post to suppliers but were not presented to the company’s bank until August 2015.

vi) The last page of a bank account paying-in book shows a deposit of GH¢1,040 which was not credited to the account by the bank until 1st August 2015.

vii) The company’s bank statement at 31st July 2015 shows a balance of GH¢318.

Required:

a) Demonstrate any adjustments needed to the company’s accounting records. (8 marks)

View Solution

b) Prepare a Bank Reconciliation Statement as at 31st July 2015. (6 marks)

View Solution

c) Explain THREE benefits to BW Ltd of reconciling its cash book and bank statement balances. (6 marks)

View Solution

- It enables missing entries in the cash book to be accounted for, preventing errors in the financial statements. For example, the bank charges and the returned cheque.

- It enables errors in the cash book to be identified and corrected, preventing errors in the financial statements. For example the transposition error and the cheque paid to the suppliers.

- It enables errors on the bank statement to be identified/investigated and notified to the bank for correction.

- It enables out-of-date cheques to be identified and cancelled in the cash book.

- It acts as a deterrent to fraud due to the bank statement being an independent accounting record prepared by the bank.