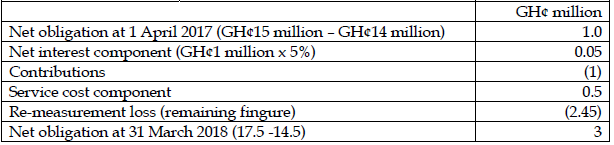

Nov 2018 Q5 c.

You are the financial controller of Navrongo Ltd (Navrongo), a company that experienced a relatively difficult trading during the year ended 30 September 2018. Reporting deadlines for the 2018 financial statements are rapidly approaching and you have a number of matters to finalise. The finance director made the following suggestion in an email:

“A revised accounting standard that is relevant to Navrongo is expected to be issued by the IASB during the 2019 calendar year. Based on the content of the corresponding exposure draft, the revisions to the accounting standard would be beneficial to Navrongo in the year of adoption. The 2018 Navrongo financial statements should be prepared using the proposed

new accounting standard on the basis of voluntary early adoption of the new standard”.

Required:

Explain to the finance director, justifying whether you agree or disagree with the suggestion above. (6 marks)

View Solution

• Although a revised accounting standard is expected to be published during 2019, it is not appropriate to implement changes in the 2018 financial statements. The revised standard has not yet been formally published by the IASB (in accordance with the

IASB’s procedures for developing and publishing accounting standards) and therefore does not yet have any standing for 2018 financial reporting purposes.

• It is not appropriate to implement financial reporting changes based on the contents of the exposure draft as comments submitted to the IASB in respect of the exposure draft may significantly affect the content of the final standard. While there may be an expectation that the revised standard will be issued in 2019, that is not a certainty and there can be significant periods of time between the exposure draft stage and finalisation of an accounting standard. Furthermore, once published, there may well

be a further period of time before the standard becomes effective.

• Early adoption of standards (prior to its stipulated effective date) is sometimes permitted and encouraged by the IASB but this does not apply to the exposure draft stage of development. On this basis, the 2019 financial year is the earliest year for which adoption of the proposed new standard is a possibility.