May 2016 Q1 a.

Your newly appointed Managing Director is preparing to deliver a paper on the need to keep budgets clean and use it as a model of change in the organisation. As the Management Accountant of your organisation, briefly explain to him;

i) FOUR differences between Zero based and Activity based budgeting. (4 marks)

View Solution

- The Zero Based Budgeting is a method where all expenses have to be justified for every new period. The Activity Based Budgeting is a budgeting method where all the activities that invite cost in all functional areas in an organisation are recorded and the relationship between them is analysed.

- In Zero Based Budgeting, all functions in an organisation are analysed for its needs and costs.

- Zero Based Budgeting can also be termed as a re-evaluation of the program and expenditures of an organisation.

- The Activity Based Budgeting aligns all activities with the objectives.

- The Activity Based Budgeting helps in effective analysis of the profit potential of an organisation’s services and its products.

ii) FOUR benefits of Activity based budgeting. (4 marks)

View Solution

- Different activity levels will provide a foundation for the base package and incremental packages of Zero Based Budgeting.

- It will ensure that the organisation’s overall strategy and any actual or likely changes in that strategy will be taken into account because it attempts to manage the business as the sum of its interrelated parts.

- Critical Success Factors will be identified and performance measures devised to monitor progress towards them.

- Because concentration is focused on the whole of an activity, not just its separate parts, there is more likelihood of getting it right first time. For eg what is the use of being able to produce goods in time for their despatch date if the budget provides insufficient resources for the distribution manager who has to deliver them.

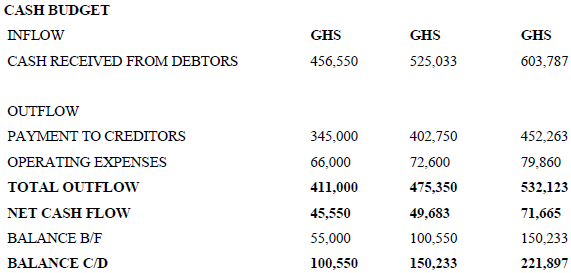

iii) FOUR advantages of using cash budget as a management control tool. (4 marks)

View Solution

- This tool helps determine whether cash balances remain sufficient to fulfil regular obligations and whether minimum liquidity and cash balance requirements stipulated by banks or internal company regulations are maintained. It also helps a company determine whether too much cash is retained that could be otherwise used in productive activities. Companies that borrow from banks need to monitor their cash coverage ratio and preparing a cash budget constitutes the first step in calculating this ratio.

- Cash budgets identify the amount of cash required to fulfil immediate, short-term obligations without utilization of overdraft protection or lines of credit. Businesses use this information to determine the extent of credit sales. Offering credit and extending credit periods usually increases sales. A company with excess cash can afford to sell on credit and thereby boost profitability. Conversely, a company hard-pressed for cash might decide to sell products at discounted prices for cash. Offering such discounts may be cheaper than the cost of overdraft fees or credit interest.

- Companies use cash budgets to make plans for optimal utilization of cash. The goal is to retain only the minimum required working capital, investing the surplus cash in productive ventures, such as making profitable investments, expanding production capacity, purchasing raw materials in bulk and in using cash to obtain favourable discounts. Companies hard-pressed for cash can take many steps to improve their position, such as reducing credit sales, postponing or reducing dividends, collecting credit early, rescheduling debt repayment and other pay-outs, cutting back on manufacturing products that require resources but do not yield much cash in the short term, and so on. Companies also look at a cash budget to determine the extent of cash available, if any, to finance capital expenditures.

- Preparing a cash budget sheds light on where cash goes. Individuals and companies can analyse each item of expenditure to determine the purpose of such expenditure and the value received in return for the expense. This allows them to cut down on unproductive expenses, bring in financial efficiency, and improve the quality of financial decisions.