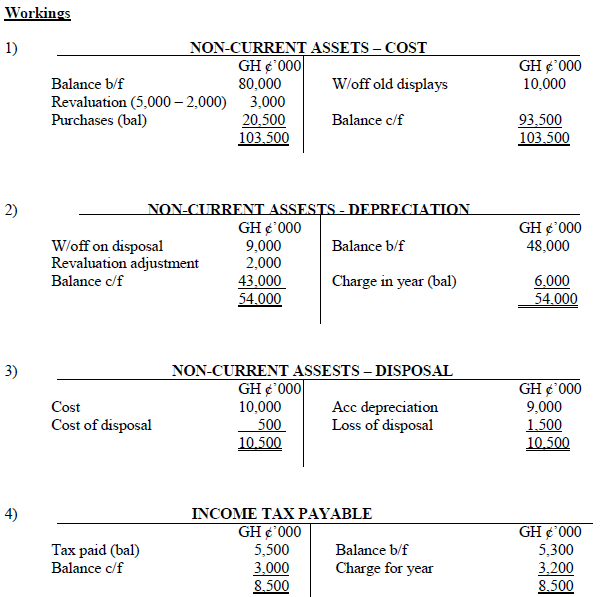

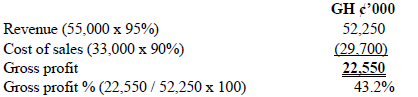

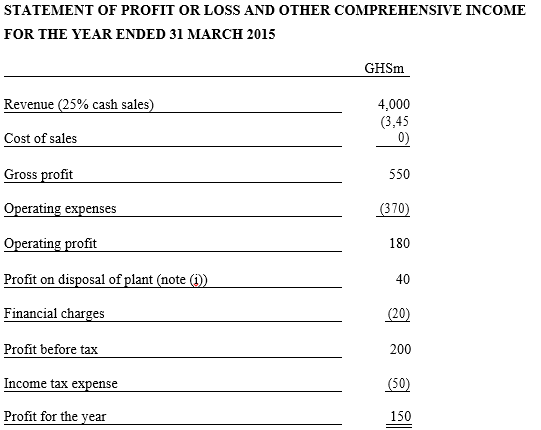

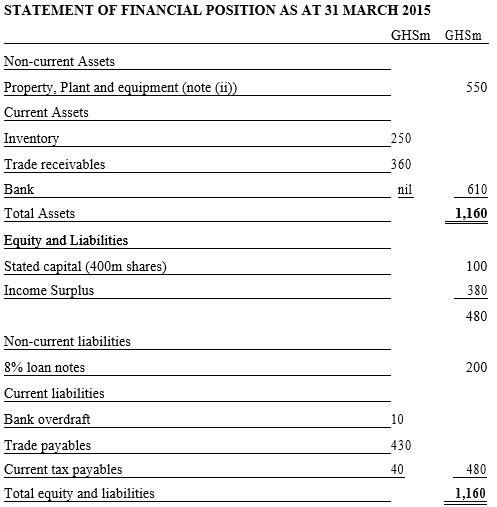

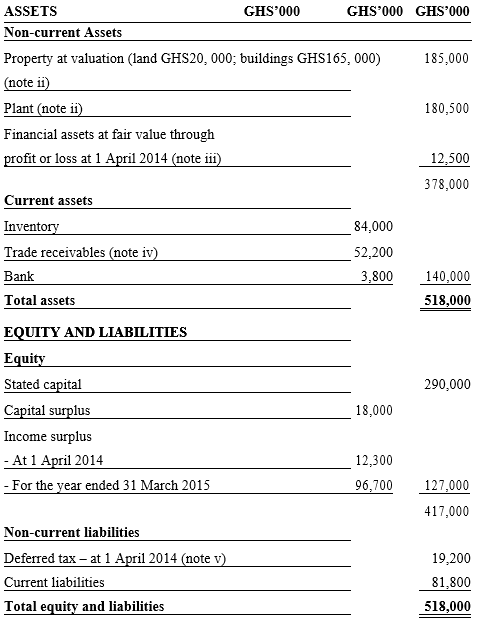

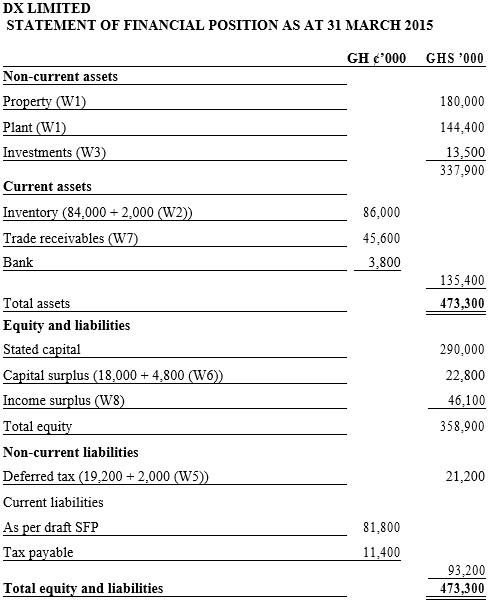

Nov 2015 Q4 b.

LB Ltd is a construction contract company involved in building commercial properties. Its current policy for determining the percentage of completion of its contracts is based on the proportion of cost incurred to date compared to the total expected cost of the contract.

One of LB Ltd’s contracts has an agreed price of GHS500million and estimated total costs of GHS400million.

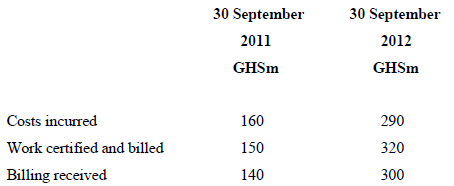

The cumulative progress of this contract is:

Year ended:

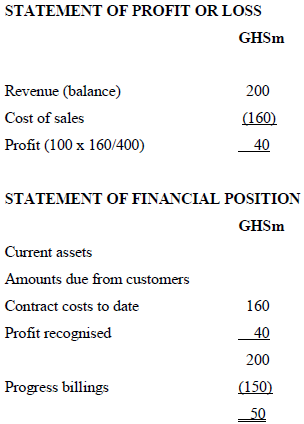

Based on the above, LB Ltd prepared and published its financial statements for the year ended 30 September 2011. Relevant extracts are:

Contract receivables (150-140) 10

LB Ltd has received some adverse publicity in the financial press for taking its profit too early in the contract process, leading to disappointing profits in the later stages of contracts. Most of LB Ltd’s competitors take profit based on the percentage of completion as determined by the work certified compared to the contract price.

Required:

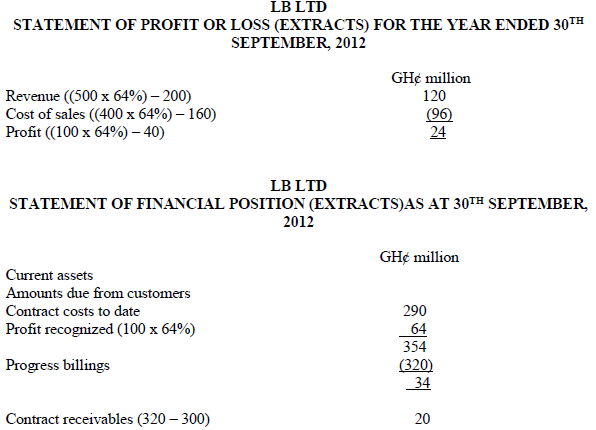

(i) Assuming LB Ltd changes its method of determining the percentage of completion of contracts to that used by its competitors, and that this would represent a change in an accounting estimate, calculate equivalent extracts of profit or loss and statement of financial position for the year ended 30 September 2012. (7 marks)

View Solution

Based on value of work certified, the contract is 64% complete ((320 / 500) x 100) at 30 September 2012. Extracts for 2012 are:

(ii) Explain why the above represents a change in accounting estimate rather than a change in accounting policy. (2 marks)

View Solution

Accounting policies are the rules, principles and practices adopted by an entity in preparing its financial statements. They should be based upon IFRSs or other financial reporting standards.

Accounting estimates are the measurements and valuations arrived at by an entity in applying accounting policies to specific items and transactions.

In the case of LB Ltd, the accounting policy is in accordance with IAS 11 Construction Contracts. Revenue and costs are recognized according to the stage of completion of the contract. LB’s current means of estimating the stage of completion is based on proportion of cost to date to total cost.

Although the question refers to it as LB’s ‘current policy’, this is an accounting estimate, because it is LB’s method of applying the accounting policy. A different measurement basis, based on the same accounting policy, is to estimate stage of completion based on the value of work certified. In transferring from one to the other, LB is making a change of accounting estimate.